The surprising results of an Aquin study by Martin Kanatschnig, Dr. Kurt Gerl, Raphael Muth and Jana Dillmann

I am sure you have often wondered: why are some lighting companies so successful and others are not? Even if they seem to work in the same sector of light? We have been advising on company acquisitions for 14 years and involved in 16 transactions in the lighting sector in Europe. Investors have asked us this question time and time again.

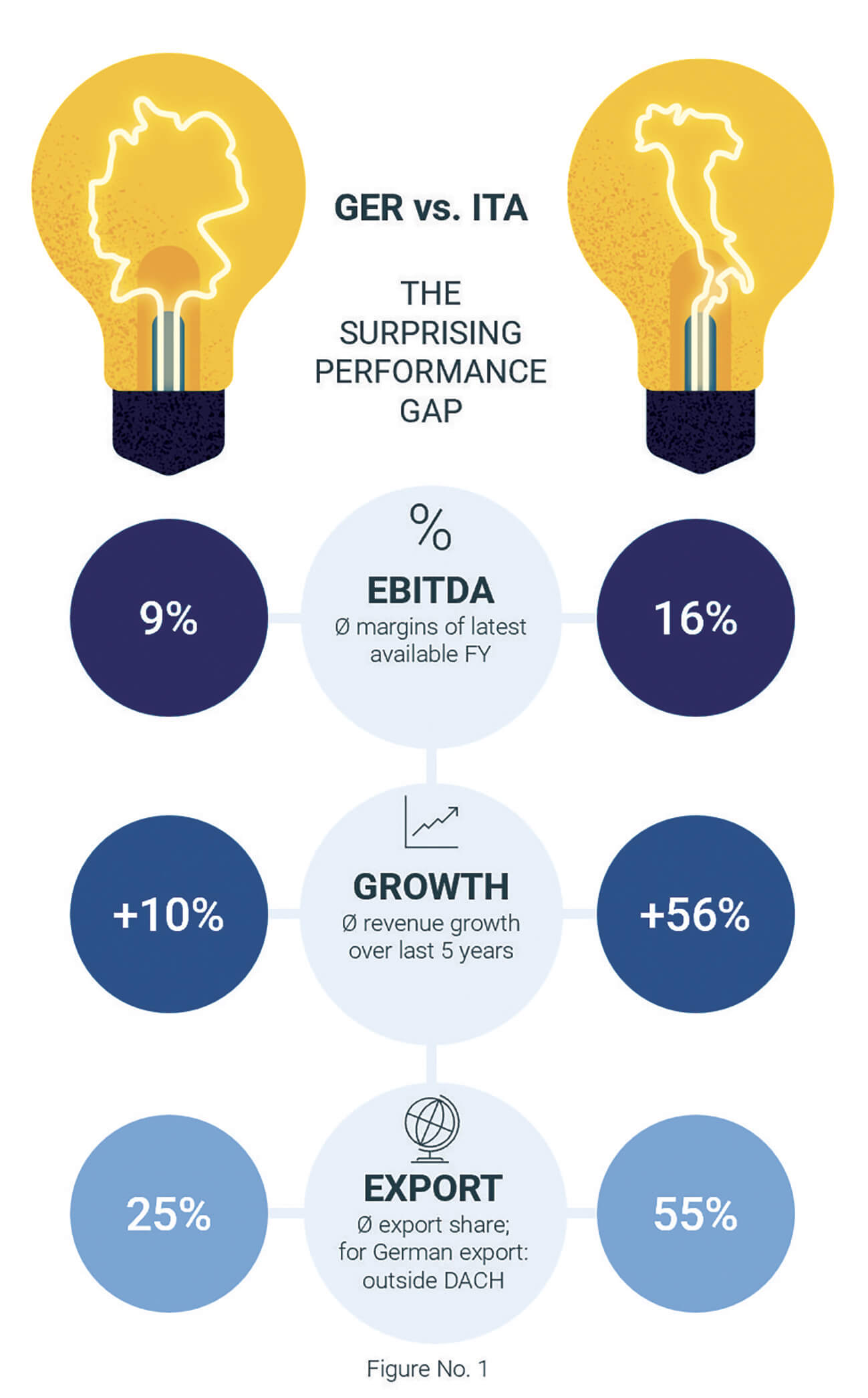

Even before we found a new owner for Ingo Maurer at Foscarini, we were in contact with numerous Italian lighting companies and could visit some directly on-site. We were frequently surprised by how well they were doing economically. It prompted us to perform a comparative study between Italian and German lighting manufacturers, including Austrian companies. Despite our predictions, the results were astonishing: Italian lighting manufacturers are almost twice as profitable as their German counterparts!

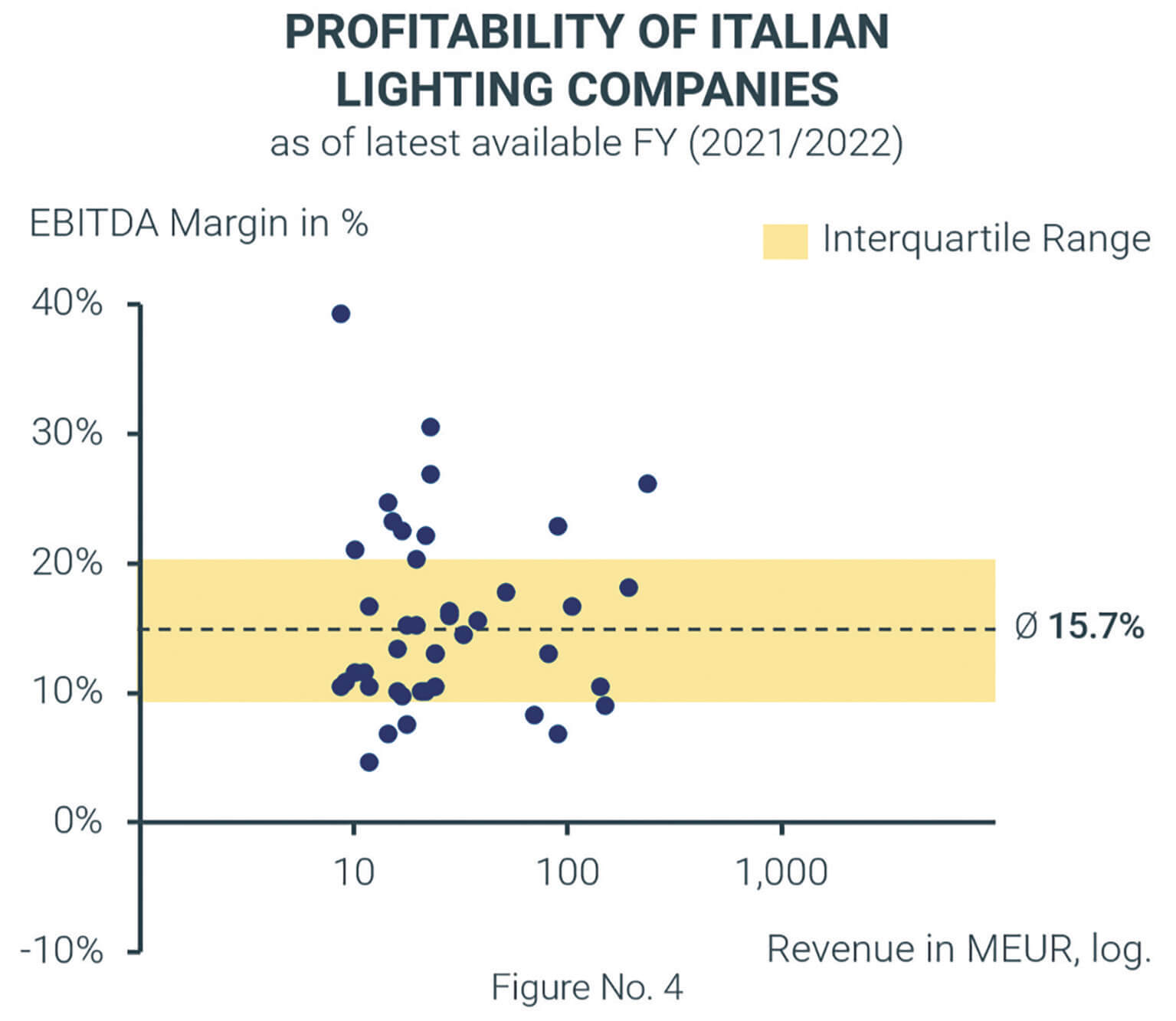

The Italian manufacturers’ gross average operating margin (EBITDA) was 14.9%, while their German counterparts reached only 7.7%. The average profitability data, which is slightly higher due to individual extremes, is shown in Picture 1. The Austrian lighting manufacturers are geographically located between the two countries, and so is their gross average operating margin (EBITDA) that lies in the middle, at 11.0 per cent.

In addition, Italians have grown by more than 50% in the last five years, while German lighting manufacturers have only managed to achieve 10% growth.

We were also surprised by the export quotas of lighting companies from both countries. Germans sell an average of about a quarter of their products to non-German-speaking countries, while the Italians’ export share surpasses 50%. Among German producers, we hear how difficult it is for them to grow internationally.

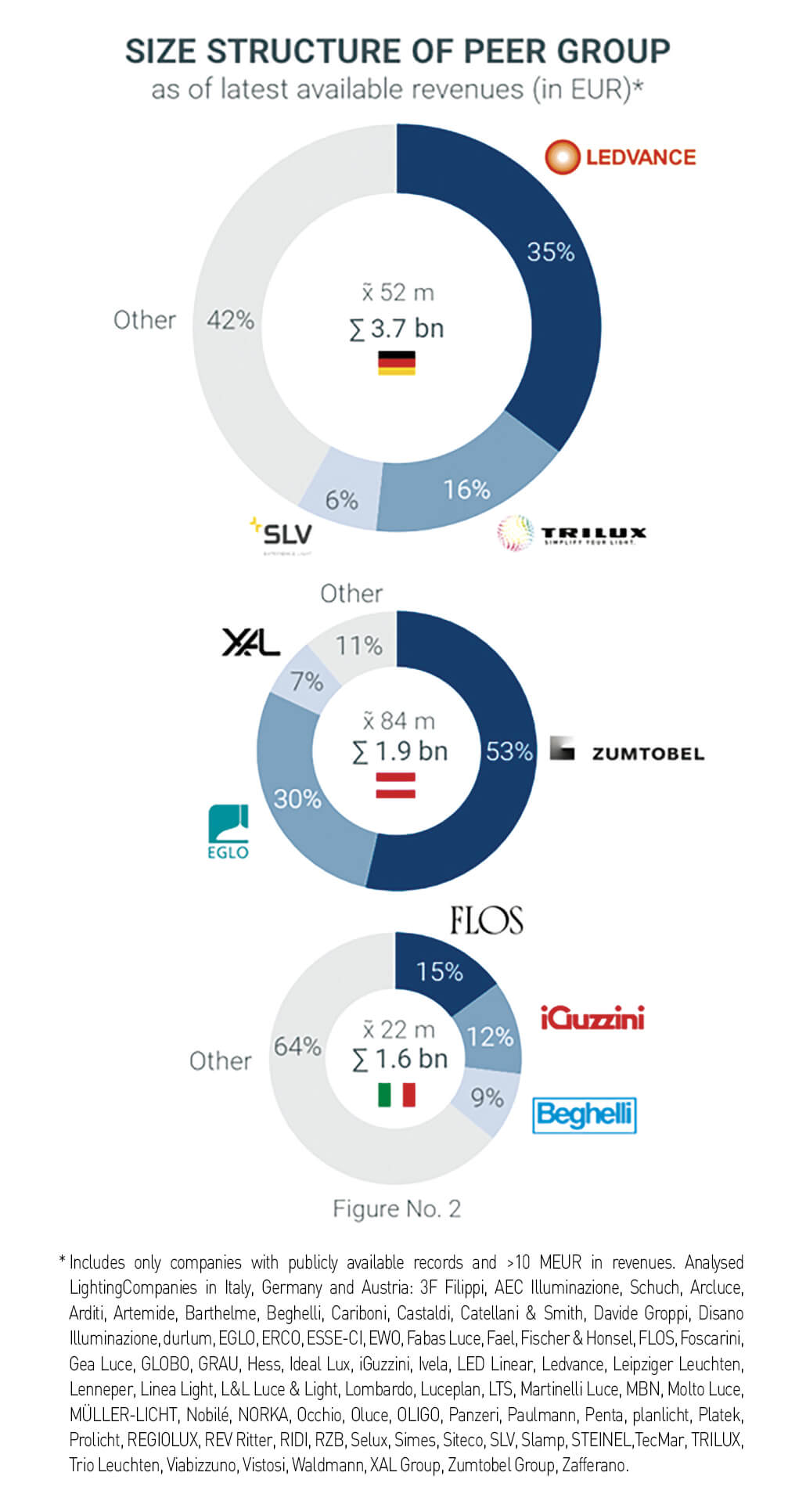

Before we attempt to provide a convincing explanation for this “Italian miracle“, we would like to summarise how we got there. We analysed our extensive database and accessed the public sources that referred to the European lighting landscape. We examined the annual financial statements of 37 Italian, 30 German and 7 Austrian lighting manufacturers. As selection criteria, we used turnover (higher than 10 million euros), segments (excluding components and niche applications) and, necessarily, data availability (German companies are far less transparent than Italian ones). In the footnote to Figure 2 are the names of the evaluated companies – in our opinion, a representative sample.

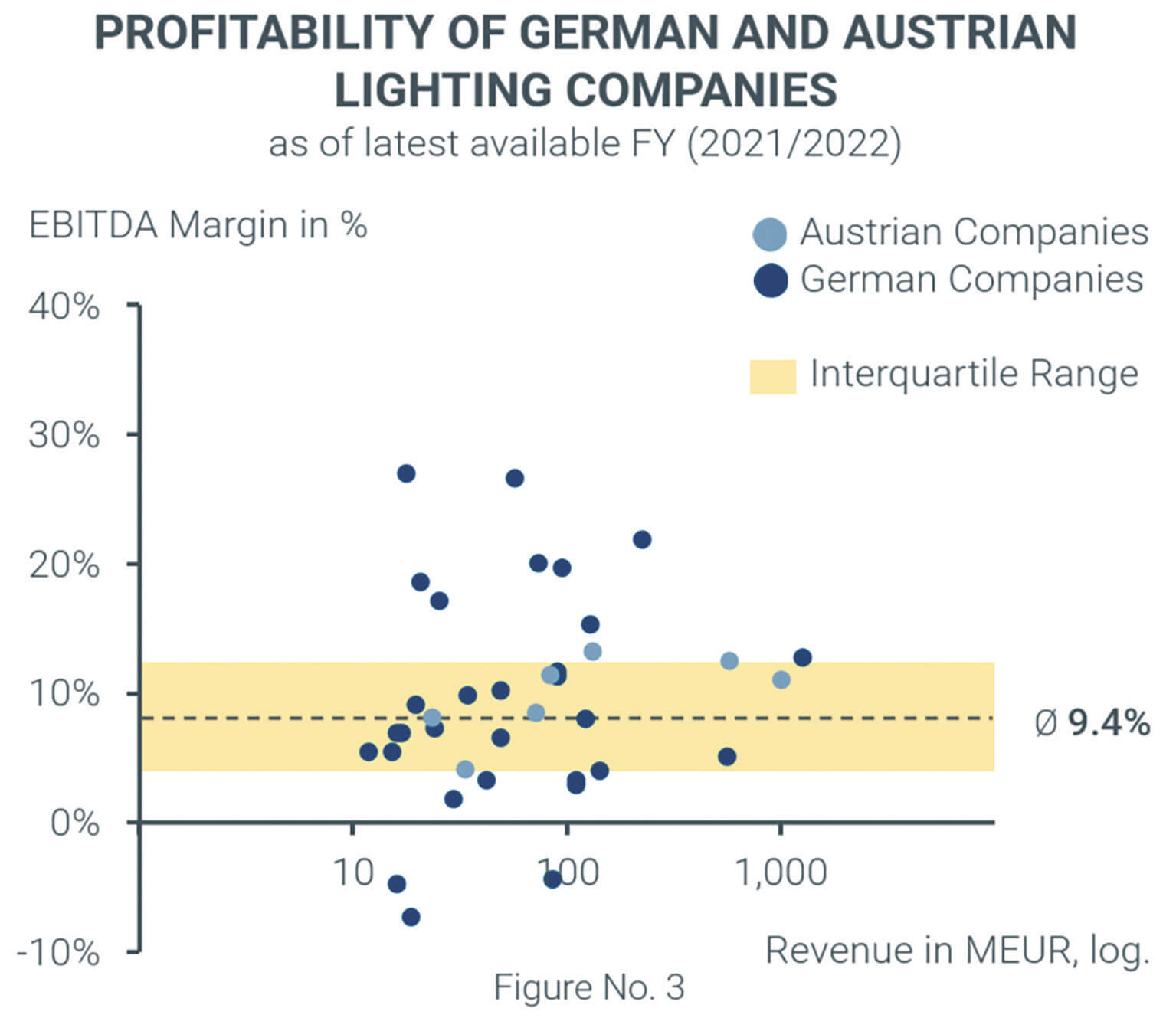

To find out the main reasons for these sensible differences, we tested the “usual assumptions”, starting with the size of the companies. However, as shown in Figure 2, both German and Italian lighting markets are fragmented and featured by medium-sized companies. Even if the two comparison groups looked different in revenue size, as shown in Figures 3 and 4, this criterion does not offer additional insights. In the three examined Countries there is no significant correlation between size and profitability – which is also a remarkable finding.

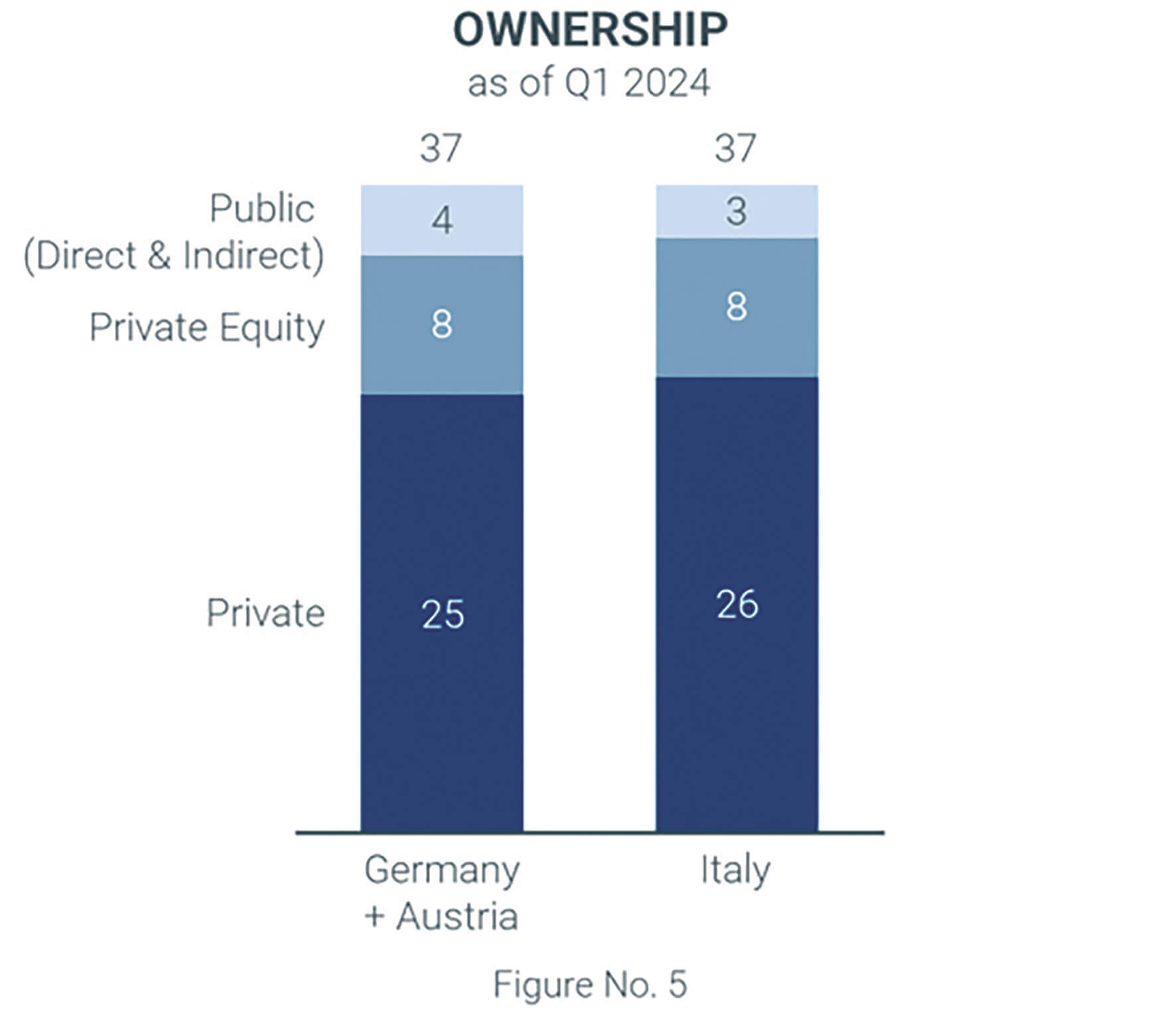

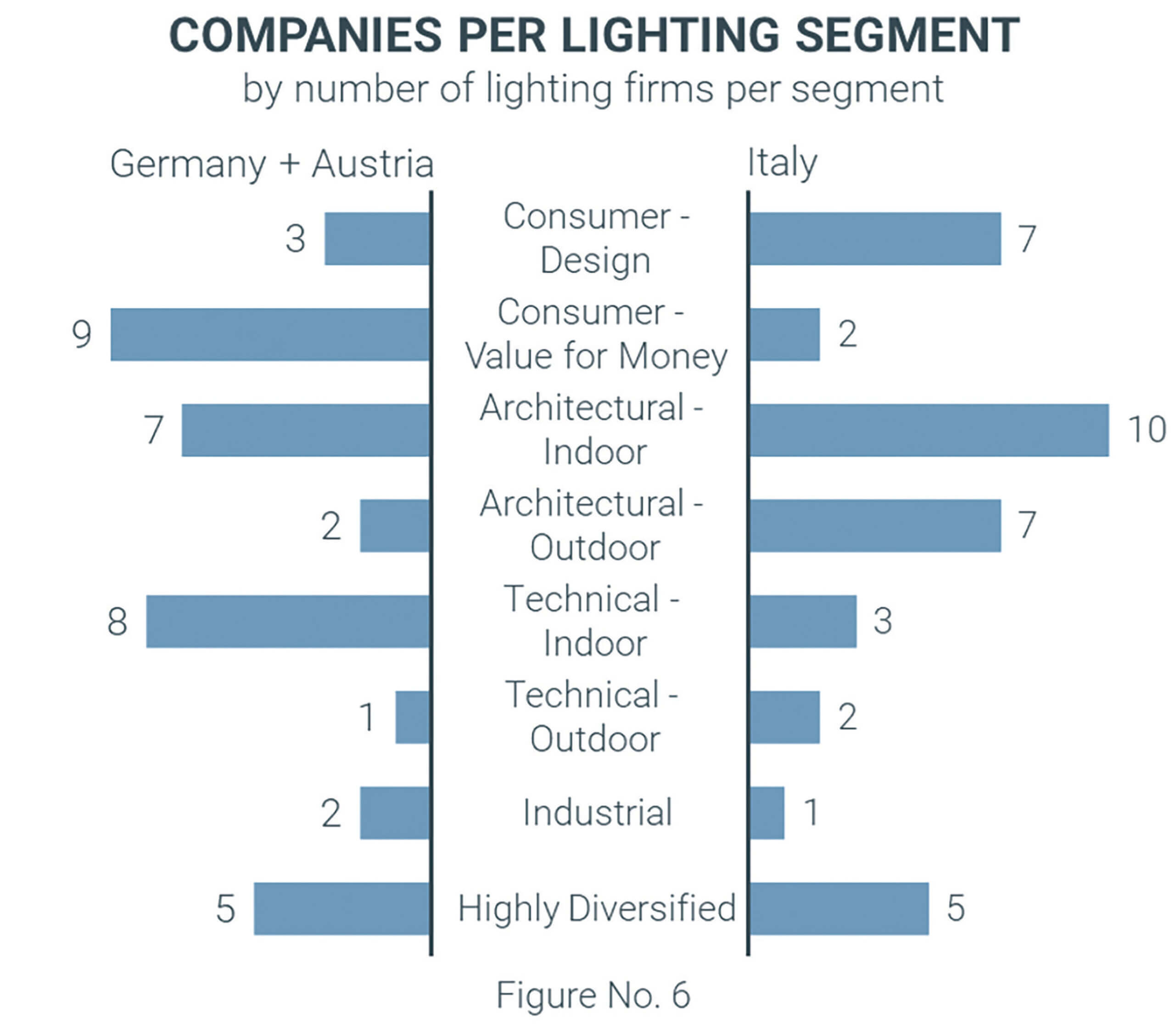

Another “suspect” criterion was the ownership structure. Are there any structural differences? In Italy, are there more companies owned by financial investors that demand higher margins and growth rates more strongly? But, again, we found nothing: The proportion of privately owned companies is comparably high in Germany as in Italy (Figure 5). But what are the “actual” reasons? The structural differences become apparent by looking at Illustration 6, which classifies companies according to different lighting application segments. German luminaire manufacturers have made a name for themselves with their high technical quality. With the aim to stay competitive, despite the rising labour cost, they heavily invested in mechanical equipment, but Chinese and Eastern European competitors have caught up in quality. Above all, in the “commodities” sector, German companies are under heavy pressure. Technical quality itself is no longer a unique selling proposition (USP).

Italy is particularly competitive when it comes to architectural design and lighting. As it turns out, a good design is very individual and competitors from low-wage countries cannot easily copy it. Mastery of this art has become a prerequisite for achieving attractive margins and export success. Our data confirm this hypothesis. Design-oriented German companies with unique lighting solutions tend to achieve better margins than those focusing on high-volume technical lighting. The latter are increasingly sourcing core products from China or Eastern Europe.

Do employees in Brescia have lower salaries than those in Sauerland? Yes, but this effect is not decisive. On average, Italian lighting manufacturers based in northern Italy have a personnel cost of €53,000 per employee, compared to €58,000 for their German counterparts. What appears most important is that Italians have a lower vertical range of production than Germans. In addition to investing heavily in local production automation, they have already made their production set-up more flexible at an earlier stage and have gained remarkable experience in procuring (preliminary) products.

This means that fewer employees work for the same output. The Italians generated 420 thousand euros in turnover per employee, while the Germans only had 250 thousand euros.

Our conclusion for German manufacturers: It seems that greater personalisation of the product range helps to improve profitability. Far from pure domestic mass production (in Germany). An increased focus on exports also seems to have a very positive effect. Since both strategies cannot be implemented organically by most German lighting manufacturers – anyway very slowly – active acquisitions in other European countries are an option. A large number of investors are willing to support the development stages if they don’t have the liquid funds and experience to do so.

Our conclusion for Italian manufacturers: the German market holds the most relevant European sales potential. With a few exceptions, Italian lighting manufacturers struggle to establish themselves in Germany despite export successes. A merger with a well-established German lighting company with a strong presence in the market and distribution channels could prove to be a promising strategy. At this year’s Light & Building trade fair, we heard from several Italian companies in the lighting industry that are actively looking for German companies for the first time. The economic success of recent years has provided them with significant liquidity reserves.

Aquin & Cie. AG, München

Article published on Highlight, Mar/Apr issue

* Includes only companies with publicly available records and >10 MEUR in revenues. Analysed LightingCompanies in Italy, Germany and Austria: 3F Filippi, AEC Illuminazione, Schuch, Arcluce, Arditi, Artemide, Barthelme, Beghelli, Cariboni, Castaldi, Catellani & Smith, Davide Groppi, Disano Illuminazione, durlum, EGLO, ERCO, ESSE-CI, EWO, Fabas Luce, Fael, Fischer & Honsel, FLOS, Foscarini, Gea Luce, GLOBO, GRAU, Hess, Ideal Lux, iGuzzini, Ivela, LED Linear, Ledvance, Leipziger Leuchten, Lenneper, Linea Light, L&L Luce & Light, Lombardo, Luceplan, LTS, Martinelli Luce, MBN, Molto Luce, MÜLLER-LICHT, Nobilé, NORKA, Occhio, Oluce, OLIGO, Panzeri, Paulmann, Penta, planlicht, Platek, Prolicht, REGIOLUX, REV Ritter, RIDI, RZB, Selux, Simes, Siteco, SLV, Slamp, STEINEL,TecMar, TRILUX, Trio Leuchten, Viabizzuno, Vistosi, Waldmann, XAL Group, Zumtobel Group, Zafferano.