In 2021, the value of the Smart Home exceeded pre-pandemic levels, despite the shortage of semiconductors and raw materials that led to 75 million euros losses in sales.

Household appliances (21%), smart speakers (20%) and security solutions (19%) lead the market. The eRetailer race continues (+20%), and the traditional supply chain is also recovering (+40%). 74% of consumers have heard of “Smart Home”, and 46% own at least one of the smart objects.

These are the results of the research undertaken by the School of Management of the Politecnico di Milano on the Smart Home of the Internet of Things Observatory, presented on 18/02 during the conference “The Smart Home starts running again and opens the door to services”.

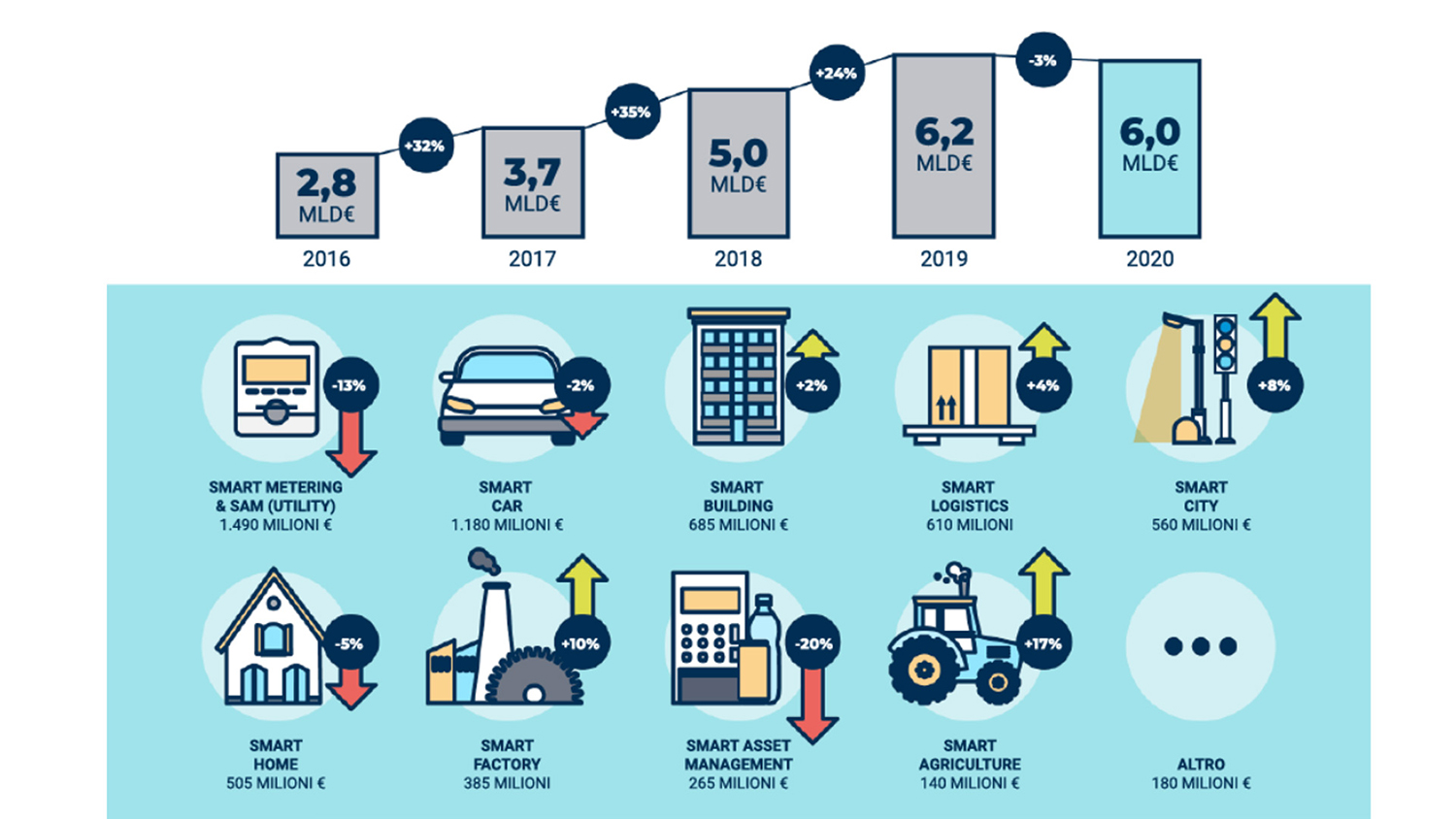

2021 was the year of revival for the Smart Home in Italy. The market started to work again, +29% compared to 2020, reaching 650 million euros, equal to 11 euros on average per inhabitant, even surpassing pre-Covid levels. Despite the encouraging results, the growth could have been higher (+45%) without the shortage of semiconductors and raw materials, which accounted for 75 million euros in loss of sales.

The products driving the market are mainly: connected appliances (135 million euros), smart speakers (130 million euros), security solutions (125 million), boilers, thermostats and air conditioners connected for heating and air conditioning (110 million), followed by audio boxes, bulbs, smart plugs and devices remotely to manage curtains and shutters. However, the Italian market remains far from the top ranking at the European level. The United Kingdom (€4 billion, +43%, €58.7/inhabitant) and Germany (€3.9 billion, +37%, €46.8/inhabitant) pass, while Italy shortens the distances from France (€1.3 billion, +16%, €19.4/inhabitant) and increases its distance from Spain (€480 million, +14%, €10.1/inhabitant).

The general public increasingly knows the concept of the Smart Home. 74% of consumers have heard of it at least once (69% in 2020, 68% in 2019, 59% in 2018). And 46% of Italians own at least one of the smart objects at home, a figure in constant growth compared to the previous three years (43% in 2020, 42% in 2019, 41% in 2018. 2021 shows a remarkable increase in sales and the best recovery for the traditional supply chain (+40%, 245 million euros). This is thanks to state incentives (Ecobonus above all), the eRetailers who continue to ride the push to online purchases (+25%, 225 million euros), and the multichannel retailers showing a recovery from the decline by Covid (125 million euros, +29%).

The market – In 2021, the Smart Home market in Italy recorded a high growth rate (+29%) compared to 2020, reaching a share of 650 million euros (11€/inhabitant). Household appliances lead the market with a share of 21% (135 million euros) and a growth rate of +35%, thanks to a progressive expansion of the offer and sales boom of some types of small household appliances such as robot vacuum cleaners and air purifiers. Then the smart speakers, a sector worth 130 million euros (20% of the market, +25%), in which purchases are increasingly oriented towards devices with displays, 25% of the speakers sold in 2021, 40% in terms of value.

However, much remains to be done to enable proper integration with the Smart Home. In Italy, only 11% of smart speaker owners use these devices to manage different smart objects at home. Substantial recovery for the security solutions, with their third place in the market (19%, 125 million euros), with a +20% growth that does not yet allow to fill the gap compared to 2019. The hardware solutions such as video cameras, sensors for doors/windows and connected locks drive the market. And this happens despite the multiple offers linked to subscriptions allowing to store images and videos on the cloud, make automatic emergency calls or activate emergency services in the event of an alarm. Among the reasons that would contribute to buying smart objects in the future (44% of respondents), the consumers place the increase in home safety first.

Connected boilers, thermostats and air conditioners for the management of heating and air conditioning follow with 110 million euros (17%, +45% compared to 2019) in terms of incidence on sales. That is the most growing area in the market, particularly favoured by the sale of numerous connected boilers, often combined with smart thermostats, which benefit from Superbonus and Ecobonus incentives, and by the possibility of obtaining benefits in terms of energy-saving and comfort. The remaining market share is made up of audio speakers (9%, +20%), light bulbs (8%, +25%), smart plugs (electrical sockets, 2%, +30%).

Sales channels – 2021 was a year of solid recovery for many sales channels. E-Retailers continued to ride the push to online purchases, observing an excellent growth rate (+25%) and reaching 225 million euros at the end of 2021 (35% of the market). Multichannel retailers and the traditional supply chain, which in 2020 had alternated between lights and shadows because of the restrictions inflicted during the year, saw a substantial recovery in 2021.

Multichannel retailers have significantly increased their turnover compared to that recorded in 2020 (125 million euros, +29%) thanks to the return of customers in stores and the growing interest in the possibility of remotely managing connected devices and appliances at home. The traditional supply chain also saw strong growth in 2021 (+40%, 245 million euros), thanks primarily to the boost given by incentives, Ecobonus above all.

Consumers – The Italians’ knowledge level about smart home devices is increasing. At the end of 2021, 74% of the Italians said they learned of Smart Home at least once (69% in 2020, 68% in 2019, 59% in 2018). And it becomes more and more of a mass phenomenon. TV advertising is the first source of knowledge for Italians (51%, +19% compared to 2020), recording a significant growth among the various sources of information available to the consumer, then the internet (34%), the word-of-mouth via acquaintances (26%) and social networks (20%). At the same time, the spread of smart objects in homes is growing: 46% of people have at least one connected device, a figure in constant growth compared to the previous three years (43% in 2020, 42% in 2019, 41% in 2018), in particular the youngest, between 18 and 34 years old (63%) and those who are more familiar with technologies (78%). The reasons for purchasing are mainly related to comfort (38%), safety (22%) and the capacity to control connected devices remotely (14%).

Technology – The evolution of enabling technologies for the Smart Home continues. In particular, in 2021, the effort of the member companies of the Connectivity Standard Alliance (CSA) was consolidated towards drafting the specifications of Matter, the new protocol for the interoperability of the Smart Home, albeit late on the timeline defined in 2020.

“The first demonstrations, presented at CES in Las Vegas at the beginning of 2022, testify to the good progress of the specifications defined to date – explains Antonio Capone, Scientific Director of the Internet of Things Observatory – and the growing maturity of the technology in support of the existing standards on the market. The first “Matter-compliant” products are likely to be expected by the end of 2022, leaving time for manufacturers to focus on defining the differential elements of related products and services to emerge in the new integrated Smart Home scenario “.